So Liverpool FC is up for sale – not just the minority stake that the club’s reviled owners, Tom Hicks and George Gillett, had placed on the market many months ago, but the whole damn thing. Liverpool’s bankers have finally run out of patience with the unpopular duo and brought in a new chairman, Martin Broughton from British Airways, with the explicit task of securing a buyer and getting a deal done. The banks may have extended the repayment date on the club’s loans, but they have made it crystal clear that they want their money back.

Displaying the customary self-assurance of Liverpool’s senior executives, Broughton confidently talked about “completing a sale within a relatively short period – a matter of months.” However, the fans have learned not to believe every statement uttered by the management hierarchy, most notably being disappointed by Rafa Benitez’s failure to deliver the fourth place in the Premier League that he had foolishly guaranteed. Specifically on the investment issue, managing director Christian Purslow’s promises to obtain £100m additional financing first by the turn of the year, then Easter, also proved to be of the empty variety.

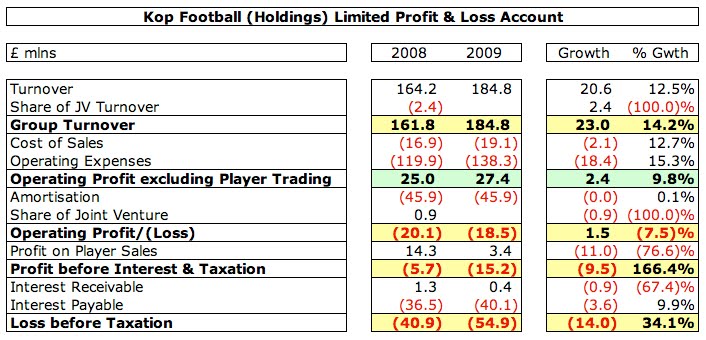

Consequently, if we want to know whether Liverpool would be a good investment, we need to stop listening to those who have a vested interest in making the sale. Instead, let’s take a look at the accounts for a truly unbiased view of the club’s financial situation. Fortunately for us, last week the club published a new set of accounts for its parent company, Kop Football (Holdings) Limited. Ideally, these would be more up-to-date, as these results only cover the twelve months up to 31 July 2009. In fact, that’s the first thing to note about these results: they’re issued late (almost a fully year after the accounting period finished), which is rarely a good sign. In fact, it’s normally an indicator of bad news.

Sure enough, the headline figure is a thumping great loss before tax of £54.9m, which is 34% worse than last year’s significant loss of £40.9m. That’s a cumulative loss of £95.8m for the last two years’ results, which would give any prospective buyer pause for thought, especially as this year’s deterioration came after a successful season in which Liverpool’s revenue was enhanced by finishing second in the Premier League and reaching the quarter-finals of the Champions League, and was also boosted by a lucrative pre-season tour of the Far East. It does not take a genius to realise that the 2010 turnover will be adversely impacted by this season’s poor results (seventh in the Premier League, not making it out of their group in the Champions League), while the 2011 revenue will be even lower, as Liverpool have not even qualified for next season’s Champions League.

You don’t have to look too far for the main reason for the record loss: almost all of it is down to the huge interest payments on the loans that the Americans took out to buy the club, which has gone up 10% from £36.5m to £40.1m. Before the current ownership regime arrived, Liverpool never paid more than £3m interest in a year, as they had no need of substantial bank loans, but they have now had to shell out a total of £85.3m in interest since the takeover in February 2007. That is money that could have been used to strengthen the squad or go towards building a new stadium, instead of effectively going to the owners. It’s even more galling, when you see that this year’s increase in interest payable is due to further finance from Kop Football (Cayman) Limited, which happens to be owned by Hicks and Gillett. Financial analysts look at the interest coverage ratio, which shows how many times interest payable is covered by trading profit. Anything below 1.5x is regarded with suspicion, but Liverpool’s trading profit of £27.4m does not cover the £40.1m interest at all.

"Glad you find it funny"

Everyone knows that the club was saddled with a mountain of debt to fund the takeover, but the really bad news is that it is increasing. Net debt shot up £51.6m in the last twelve months from £299.8m to £351.8m. That is net of £26.9m of cash, so the gross debt is even higher at £378.6m, comprising £234m of bank loans (mainly with the Royal Bank of Scotland) and £144m owed to Cayman Limited. Interest on the bank loans is at LIBOR plus 5%, while the inter-company interest is accrued at a less reasonable 10% a year. This has not yet been paid, potentially casting the owners in a good light, until you realise that it is simply added to the growing debt. Earlier this year, managing director Christian Purslow said that the debt was down to £237m, but after looking at these accounts my guess is that he was referring only to the bank loans and not including the money owed to Hicks and Gillett via their offshore company. Some newspapers reported that the total debts were £472.5m, but this is over-stated, as it includes trade creditors, accruals and deferred income.

The Cayman Limited loan is repayable on demand, though the agreement states that this cannot be progressed if it would cause the company to become insolvent, which is “kind” of the owners. Of more concern is that less than half of the £297m credit facility with RBS (£110m) is secured by letters of credit and personal guarantees from the owners, leaving the remaining £187m to be secured by the club’s assets. Supporters might argue that Liverpool’s gross debt of £378.6m is only about half of Manchester United’s debt, but United generate nearly £100m more revenue and their debt is long-term, while Liverpool’s bank loans are extremely short-term in nature. The other English club with significant debt was Arsenal, but that was used to finance the construction of a cash generating new stadium, rapidly eating into the amount owed. Chelsea, of course, are in a different ball game, as their owner has simply converted the debt into equity.

"I'll get £100m by Christmas, no Easter, errm ..."

As the auditors so clearly expressed it, the club is “dependent upon short-term facility extensions”, or relying on the bank’s goodwill, which is a very uncomfortable position to be in. The current credit facility was due for repayment on 24 January 2010, but the club failed to make the £250m payment, so the bank extended the date (by just six weeks) to 3 March. Christian Purslow had previously implied that the repayment to RBS was only due in July, but it looks like the bank was not even willing to wait that long. However, it is believed that they have granted yet another extension, this time for six months, which would mean repayment in September. No wonder Broughton wants to complete the sale in just a few months.

Hicks and Gillett extending the credit facility is a habit that started last year, when RBS forced the owners to pay off £60m of their debt to the bank in return for a one year extension. In hindsight, the criticism of Dr. Rogan Taylor, director of the Football Industry Group at Liverpool University, was right on the money: “It is little more than an expensive fix – just sticking plaster, making things more difficult for the club to progress in the long run. It is still very short term, year to year, if that.” Although the directors claim that “active negotiations are in progress to secure new financing”, they acknowledge their difficulties in the annual report, “The current economic conditions have continued to have a significant impact upon world credit markets and accordingly raising finance in this environment remains challenging.” You can say that again.

Despite these financial constraints, the wage bill has still increased by 14% (£12.4m) from £90.4m to £102.9m, thus joining Chelsea, Manchester United and Arsenal as the only clubs in the Premier League with a payroll over £100m. All the same, the wages to turnover ratio is unchanged at 56%, thanks to the rise in turnover. This is not great, but is still pretty good, though it would look much worse if the club lost the revenue from the Champions League. Oh.

"What the hell's going on?"

Even though the wage bill has grown, the value of the players has actually fallen, at least on the balance sheet, with intangible assets decreasing by £34.7m to £194.8m. Of course, the players’ value in the transfer market would certainly be higher than their net book value, but the financial reality is that the club do not have many assets. In fact, according to the balance sheet, they have less than zero, as net liabilities have increased by more than £50m to £128.5m. This is despite fixed assets increasing by £20.8m, largely as a result of investment in the planning and design of the new stadium.

That means that the club has now managed to spend £45.5m on the proposed new stadium, which is some achievement, given that it is as far away as ever from being started, let alone finished. There’s still no sign of George Gillett’s famous shovel being in the ground. If the auditors decide that this stadium is unlikely to be built, these expenses will no longer be considered an asset, but will have to be written-off. The only other “asset” the club has are accumulated tax losses of £63m, which are available to offset against future profits.

Given these figures, it should be no great surprise that KPMG, the club’s auditors, repeated their warning of a year ago of a “material uncertainty which may cast significant doubt on their ability to continue as a going concern.” The fact that last year’s accounts contained the same admonition without the club going out of existence in the intervening twelve months would suggest that this is not necessarily a doomsday scenario, but it’s still a serious issue. A similar warning was included in Hull City’s last accounts, whereupon chairman Adam Pearson proclaimed, “the supporters should rest assured the club is in no danger of going out of business or going into administration”, but his tune changed a few months later, when he admitted, “nothing could be ruled out.” Hull’s problems were magnified by the significant fall in revenue following relegation from the Premier League. Potential investors in Liverpool might just ask themselves whether non-qualification for the Champions League would have a similar detrimental impact.

The really important issue for Liverpool is whether they have enough cash to pay their bills, not just in terms of their ability to service their debts, but also to pay their players’ wages and (most importantly) their tax bills. As we have seen on numerous occasions this season, HMRC have no hesitation taking football clubs to court to recover any monies owed. Liverpool are not quite there yet, but the cash flow statement does emphasise the basic flaws in their business model. At an operating level, the club generates healthy amounts of cash (£38m in 2009), but it then needs to use all of that and more on paying interest (£29m) and capital expenditure (£51m). This leaves it with a net cash outflow of £42m, which would be even worse if the club had paid the £8m interest owed to Cayman Limited. This shortfall needs to be shored up by additional financing of £49m, which obviously leads to the debt growing even more. It’s a vicious circle.

Anybody thinking of making an investment in a company would also consider the quality of the management, though they should be mindful of one of Warren Buffett’s sagacious quotes, “When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.” Nevertheless, it’s worth taking a look at how Liverpool’s management are doing.

One of the key elements in the club’s stated strategy is to strengthen the football squad. Even though manager Rafa Benitez has frequently complained about not being given sufficient resources to compete, his much-loved facts do not appear to support this view. Since his arrival in the summer of 2004, the club has backed him to the tune of spending £249m on bringing players to the club. To be fair, Benitez has recovered £141m from player sales, but that still leaves a net spend of £109m, second only to the big spenders at Manchester City (£228m) and Chelsea (£145m). However, it is considerably more than Manchester United (£32m) and Arsenal, who actually have a transfer surplus of £26m over the same period. Given that all this transfer activity has only resulted in a mediocre seventh place in the Premier League, I would argue that this strategic objective has not been achieved.

The significant spend on new players is reflected in very high amortisation of £45.9m. The accounting treatment here is to write-off the costs associated with buying players over the length of their contracts, based on the (conservative) assumption that a player has no value after his contract expires, since he can then leave on a “free”. To place this into context, this is higher than amortisation costs at Arsenal £23.9m and Manchester United £37.6m, while it is only a little lower than Chelsea £49m.

"Give me more money - or I'm off"

The other component of players’ costs are wages, which is normally a very strong indicator of how well a team is likely to perform on the pitch. For example, this season the first three places in the Premier League were filled by the teams that respectively had the highest wage bill (Chelsea), second highest (Manchester United) and third highest (Arsenal). The only team to buck that trend was Liverpool, who finished seventh, despite having the fourth highest wage bill. To sum up, Benitez has been given an awful lot of money to spend on both transfers and wages, but the statistics indicate that he has under-performed.

But Liverpool are in a Catch-22 situation with Benitez, as the feeling is that the club would prefer him to leave, but that would endanger any stability the club might have. At a time when the manager should be planning for the forthcoming season, there is substantial uncertainty over his position. Some argue that this is due to the size of any potential severance payment, but the latest accounts show that the club is willing to do that if push comes to shove, paying out £4.3m to the former chief executive and academy coaching staff. This reputedly included £3m to Rick Parry, even though he was labeled a “disaster” by Hicks.

And yet, there is some good news in the accounts if you look beyond the headline figures. Most impressively, the club is profitable at an operating level (excluding player trading, interest, tax and amortisation), making £27.4m, which was actually £2.4m (10%) up on last year. This would have been even higher without the £4.3m exceptional severance payment.

"Can you hear the drums, Fernando?"

Benitez has also delivered a £3.4m profit on player sales (Arbeloa, Leto) following a £14.3m profit in 2008 (Crouch, Sissoko, Carson, Riise, Guthrie). A further £13.4m profit was made on sales after the accounting year-end closed (Alonso, Dossena, Voronin). Of course, this is a bit of a double-edged sword, as such good business will keep the banks happy, but no fan likes to see the team’s best players leave. For example, most would agree that Xabi Alonso has not been adequately replaced.

From a financial perspective, you could argue that the £14m increased loss before tax has been largely caused by the £11m reduction in profits from, player sales. In fact, if Alonso had been sold to Real Madrid just a week earlier, the loss would have been smaller than the previous year.

The other encouraging aspect in the accounts was the 14% (£23m) increase in turnover from £161.8m to £184.8m. There was good growth in all categories with broadcasting income rising £6.4m to £74.6m, reflecting the successful season. The £3.3m increase in match day income was particularly impressive, given that there were three fewer home games in 2008/09, but the star of the show was commercial revenue, which soared 25% (£13.5m) to £67.7m, thanks to four new partnerships. Only a curmudgeon would note that this revenue growth was all but wiped out by the £21m cost growth.

Enough about the past, is there anything Liverpool can do to make themselves more attractive financially? Well, they could try to build on last year’s growth and further increase revenue. The new commercial team have obviously not been sitting on their hands, as they have already secured some future growth, notably the new shirt sponsorship deal with Standard Chartered bank that commenced after these accounts. This is worth up to £20m a year, which would be a £12.5m uplift on the old deal with Carlsberg, though apparently a significant element depends on the team’s performance. Liverpool’s commercial revenue of £67.7m is already worthy of praise, only just behind the marketing machine that is Manchester United (£70m) and a long way ahead of Chelsea (£52.8m) and Arsenal (£48.1m), but the prospectus issued last year to investors targeted growth to £111m in the next five years, which would be mighty impressive.

"The money went that way"

Of course, it is TV revenue that has driven the growth in football clubs’ revenue and this is where the failure to qualify for the Champions League will hurt Liverpool. For the 2010 accounts, the Premier League has just published its revenue distribution, which included £48.0m for Liverpool, against £50.3m the previous year. The merit payment was lower, due to the seventh position, and the team was not shown live so many times.

We can also calculate the Champions League participation and performance fees for 2010, which come to €9.1m, as they will receive €3.8m for Champions League participation, €3.3m for group stage participation (six matches at €550,000) and €2.0m for group performance (two wins at €800k, one draw at €400k). According to the Guardian, Liverpool will also be allocated €17.6m from the TV pool, up from €10.1m the previous year. This means that Liverpool will get €26.7m from the Champions League, which is actually €3.5m more than the year before, despite not progressing as far – thanks to the increase in TV money. At current exchange rates, that is worth £23.2m and we can add another £1.9m to that for the Europa League, bringing in a total of £25.1m from Europe, compared to £20.2m last year.

Liverpool’s total TV money in 20009 was £74.6m, so if we subtract the £50.3m from the Premier League and the £20.2m from the Champions League, we can estimate £4.1m came from the FA Cup and Carling Cup. Assuming a similar amount for 2010, we can add the £48.0m from the Premier League and the £25.1m from the Champions League to give a total of £77.2m TV revenue. In other words, 3.5% higher than last year, even though the team’s performance was much worse.

Not bad, but the real problem comes in 2011 when the failure to qualify for the Champions League will begin to bite. That’s at least £25m revenue gone immediately. There might be some compensation from the Europe League, but even if you win that competition, you only get €6m, so that does not really help. As Professor Tom Cannon of Liverpool University said, “qualification for the Champions League remains the crucial factor in enabling the club to maintain income at current levels.” On the other hand, the additional £7.5m that all Premier League teams will receive for the new overseas rights deal will soften the blow to some extent.

However, the real key to unlocking Liverpool’s revenue possibilities is a new stadium. Anfield is a wonderfully atmospheric old ground, but its capacity is only 45,000, which is much less than Old Trafford (76,000) and The Emirates (60,000). According to Deloittes, Liverpool’s match day revenue of £42.5m is less than half of Manchester United (£108.8m) and Arsenal (£100.1m), while even Chelsea, whose Stamford Bridge ground is even smaller (42,000), earn more from this category (£74.5m). Liverpool only earn around £1.6m from each home match, which is significantly less than United (£3.6m) and Arsenal (£3.1m). Yes, it would cost a lot to construct a new stadium (though this could be offset by offering naming rights), but Arsenal have demonstrated that this can be a profitable move, especially if you can sell a few thousand corporate boxes. New chairman Martin Broughton agreed, “I think taking the stadium plan forward has to be in everyone’s interests. I think when you look at the financial logic, it has to happen. It’s inescapable that any new owner would not go ahead with the new project.”

The other way to improve your financials is to cut costs, which in the case of a football club effectively means reducing the wage bill, as it’s by far the largest expense. The easiest, though most unpopular, route would be to cash in on the top stars, like Steven Gerrard and Fernando Torres, which would have the added benefit of generating big money in transfer fees. The Daily Mail reported that Chelsea were preparing a £70m bid for Torres alone. The chairman has assured the fans that the club does not need to sell, “We won’t sacrifice our prize assets to reduce debts”, but the players may take the decision out of his hands, as they want Champions league football and must be unhappy with the club’s financial situation. That would be another vicious circle, as losing these players would then make it even more difficult to qualify for the Champions League.

"Enough about the debt"

This is why the only realistic way out of the financial mess is to sell the club. Over the past year the press has mentioned many possible buyers, including Saudi princes, Kuwaiti billionaires, Indian industrialists, anonymous Americans, Chinese gaming tycoons and our old friends DIC, but Christian Purslow’s deadlines for attracting investment have come and gone without success. To be fair, he was dealt a poor hand, having to convince investors to stump up for a minority stake. He was also hamstrung by Hicks and Gillett, who have consistently over-valued the club, e.g. recent reports mentioned an absurd valuation of £800m. However, one positive side-effect of not qualifying for the Champions League should be a reduction in the price. Furthermore, the Financial Times reported that Broughton has been given “a casting vote on all board issues, including the planned sale.”

Liverpool will have to be careful not to jump from the frying pan into the fire by finding a new owner that would also burden the club with debt. Broughton is aware of this, “It has to be the right owners and also the right financial structure – no more than a reasonable amount of debt that you would expect in any organisation of this size.” It is clear that a new owner would require very deep pockets, but how much would he need? That obviously depends on how much Hicks and Gillett want. The Americans borrowed £300m initially in 2007 (£185m to buy the shares including fees plus £113m working capital), but as we have seen the net debt has risen to about £350m, so a price of £400m would provide them with a tidy £50m profit, which is not too shabby.

"Martin Broughton - he'll take more care of you"

In addition, finance expert David Bick said that a new owner would “need to have access to very large sums of money to build the new stadium, revitalise the management and allow for strengthening of the playing squad.” A new stadium would cost at least £300m (maybe more); the transfer budget required to improve the current under-performing team could be as much as £100m (Torres said that Liverpool were “four or five class players” short of a successful side); while changing the management might cost £15m. If any of this is funded by loans, the owner would also require sufficient working capital to service the debt. When you add all this up, we are not far short of a billion, so millionaires need not apply.

Surely Liverpool are too big to fail? That’s what they said about Lehman Brothers before it went bust. There’s no doubt that the accounts make for awful reading, which was confirmed when the Premier League asked Broughton to provide assurances that the club would be able to fulfill its fixtures next season. RBS also offered assurances that they would continue to support the club until a sale is finalised, but this was only after: (a) Hicks and Gillett reduced the bank loan by paying in more of their own money; (b) Barclays Capital were hired to find a buyer. Now that the bank loans have been trimmed, the bank is unlikely to let the club go broke, especially as it is up for sale. It is also unlikely that a bank would take the unpopular step of cutting off Liverpool’s support, though it is not so long ago that Barclays made a stand over Southampton’s overdraft, ultimately pushing them into administration.

"Kop that"

However, at the risk of stating the obvious, Liverpool are not Southampton. We are talking about one of football’s great institutions with an incredible history: winning the Champions League and European Cup five times, the English League championship eighteen times and the FA Cup seven times. In marketing terms, it is still one of the leading global football brands, playing in the richest domestic club competition in the world. It surely cannot be time to say “good-bye”, but are Liverpool a good buy? Many people would not want to invest their hard-earned money, but if a wealthy benefactor had a spare billion, he just might.

No comments:

Post a Comment